Key takeaways:

- Investing via a corporate investment account can come with benefits that could include lower initial taxes, letting you access a greater amount of capital for investing, maximizing the potential distance your corporate earnings can go, and, depending on the structure of your corporation (e.g. holding company (HoldCo) vs. operating company (OpCo)), can help segregate investment assets from operating risks.

- Deciding whether to invest via your corporation or personally can be based on your cash flow needs, long-term financial goals, and tax planning.

- Private alternative investments, like Skyline’s real estate investment trusts (REITs) and Skyline Clean Energy Fund, can provide further benefits and reinvestment opportunities that can supercharge and compound long-term corporate investing for maximum potential earnings.

Building a business requires grit, determination, and a deep commitment to overcoming obstacles and pushing to reach the next level. And when you achieve the goal of turning a healthy profit and having excess post-tax earnings to manage, choosing the right strategy for those funds could be the difference between living comfortably or living out your dreams.

Don’t just leave your corporate earnings parked in your business—if you invest your retained earnings, you can put them to work in the background, helping you focus on what’s important—the day-to-day of your business operations. And when it comes to deciding whether it’s better to invest personally or through a corporation, you just need to evaluate a few factors, like cash flow needs, long-term financial goals, and tax planning. Whichever investment path you decide on, leveraging corporate investing as part of your overall financial plan can help you pull your earnings out of the slow lane. Shift your wealth into the next gear and work to maximize its growth potential with corporate investment accounts.

How corporate investing works

Investing through a corporation is one of the ways you can utilize any corporate earnings, which is the amount you have left over from your profits after you deduct corporate tax. Corporate investing is the same as personal investing, except the ownership of the investments is your business instead of you personally. Just like personal investments, corporate investments have their own set of benefits and advantages that when strategically implemented can maximize your earning potential. When you invest your retained earnings through your corporation, you can:

- Access a greater initial amount of capital, bolstering your overall earning potential

- Defer personal income taxes, letting you strategize when you draw down salary or dividends from your corporation

- Leverage a notional tracking Capital Dividend Account (CDA), which gives you the potential of future capital dividend withdrawals that are generally tax-free

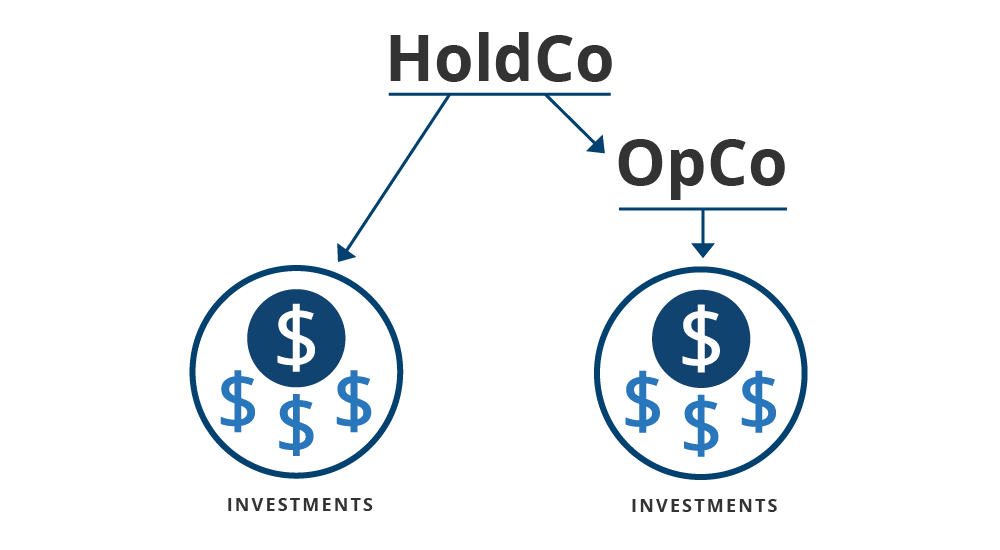

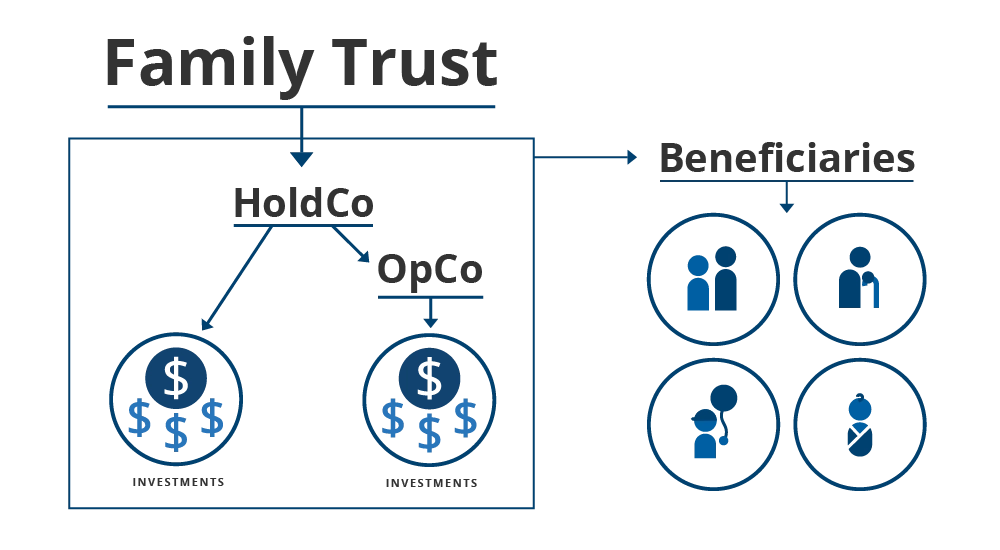

Depending on your corporate structure, you can invest directly from your operating company (OpCo), holding company (HoldCo), or even family trust.

Corporate vs. personal investing in Canada

The biggest difference between investing personally and investing through a corporation or HoldCo in Canada is taxation, specifically when and how much tax you will pay. Generally, corporate tax rates are lower than personal marginal tax rates, which means it can often be a more financially strategic decision to retain your excess earnings in your corporation and directly invest them via your business instead of drawing down salary or dividends from these funds.

Keep an eye on Small Business Deduction limits

Corporate investing in Canada can affect Small Business Deduction limits if passive income earned from those investments hits certain thresholds. Speak to a corporate tax expert to determine how to strategize corporate investment in your overall financial plan.

To determine whether or not you should retain your profits in your corporation for investment or pay them out to yourself via salary or dividends, you can calculate whether or not you will have a Retention Advantage or a Retention Disadvantage by keeping them in your company. If you have a Retention Advantage, you may want to consider corporate investment, as you will have more capital to invest upfront after paying corporate tax compared to withdrawing the same amount of money as salary or dividends and investing it after paying personal tax.

Let’s take a look at an example of a Retention Advantage.

Retention advantage in action

For this example, we are going to assume that our business owner is located in Ontario, has $100,000 in pre-tax profits they would like to invest for retirement, and is at the top marginal personal tax rate.

Scenario 1: They can withdraw the $100,000 as a bonus and lower the amount of corporate tax they would have to pay. At the top marginal tax rate, which is around 50%, they would have to pay approximately $50,000 in personal income tax, leaving them with about $50,000 to invest.

Scenario 2: They retain the money in the corporation and pay corporate tax on the amount. If the company is eligible for the Small Business Deduction (SBD) rate, which is around 12% in Ontario, they would have to pay approximately $12,000 in corporate taxes, leaving them with about $88,000 to invest via their corporation. If their business did not qualify for the SBD, they would have to pay the general corporate tax, which is around 26.5%. This means they would have to pay approximately $26,500 in corporate tax, leaving them with about $73,500 to invest via their corporation.

As we can see, in either corporate tax situation of Scenario 2, the business owner would have more money upfront to invest if they retained the amount in their corporation versus if they paid out the amount as part of their salary and then invested the remaining post-tax amount. This is a Retention Advantage.

Bottom line: having a blend of personal and corporate investment accounts as part of your overall portfolio can be an integral part of a strategic financial plan. Talk to an advisor about your financial goals to make sure you’re maximizing the most tax efficiencies.

How can I maximize corporate investing with private alternatives?

1. Take advantage of capital gains returns

Besides the greater amount of funds you might have access to by investing your excess corporate earnings directly through your business, the biggest advantage of corporate investing is being able to potentially draw down tax-free dividends from a CDA, giving you cash flow without affecting your overall personal marginal tax rate. By focusing on investments that deliver returns as capital gains, your corporation can continue to grow its wealth efficiently.

Private alternative investments, like Skyline’s REITs, can be a strategic choice for achieving these gains. When your corporation receives returns, it pays corporate tax on only 50% of the amount, while the untaxed portion is added to the CDA, giving you the opportunity to access these funds later, tax-free. It’s important to note, though, that while only 50% of capital gains returns earned through your corporation are taxable, those returns can be taxed at higher rates upfront, with part of the amount charged potentially refundable when taxable dividends are paid out from your corporation.

2. Target Return of Capital (RoC) distributions

Investments that pay out Return of Capital (RoC), are also tax-efficient choices for your corporate investment portfolio. RoC is not considered income, so it doesn’t initially trigger either corporate or personal income tax; however, it does reduce the adjusted cost base (ACB) of your initial investment amount, and this could lead to increasing the capital gains amount when the investment is ultimately sold and potential penalties if the ACB drops below zero. Even with these implications, returns classified as RoC offer tax efficiency that other high-taxed returns don’t, like interest income. Consider including private alternatives that classify returns as either capital gains or RoC, like Skyline’s REITs in your corporate portfolio for maximum potential cash flow opportunities.

3. Diversify with investments backed by real assets

Private alternatives also help diversify your corporate portfolio to potentially buffer investments from being adversely affected by public market uncertainties. And when you select private alternative investments that are anchored with real, tangible assets, like Skyline’s REITs and Skyline Clean Energy Fund, you are potentially adding another layer of protection against volatile market swings, helping you achieve your financial goals that much sooner.

4. Reinvest returns for even more potential gains

Investments with Dividend or Distribution Reinvestment Plans (DRIPs) can make any returns work even harder for you. When your corporation enrolls in a DRIP, any returns from the investments are automatically reinvested, and, while those reinvested returns are still taxed since they are not held in a registered investment account, enrolling in a DRIP can increase the capital invested and maximize the power of compounding. All of Skyline’s REITs, including Skyline Apartment REIT, Skyline Industrial REIT, and Skyline Retail REIT, offer DRIPs, ensuring each dollar earned can be maximized to its full potential.

And when you invest in Skyline Clean Energy Fund, instead of receiving monthly distributions, cash is automatically reinvested into existing or new opportunities within the Fund’s mandate, allowing investors to benefit from the potential effects of compounding over time.

Next steps

Ready to get your retained earnings in the fast lane and accelerate your wealth through corporate investment with Skyline? You can get started today by following these simple steps:

- Book a meeting with a Skyline Relationship Manager to discuss your investment needs.

- Work with us to transfer or open a corporate non-registered account.

- Determine which Skyline private alternative investment products best align with your wealth goals.

- Enjoy the potential of passive income, compounding returns, and the foundational wealth you can build upon.

Life goes by fast, especially when you’re running your own business. With Skyline, you can make sure your wealth’s in the driver’s seat, taking you—and your financial goals—where you want to go.